.svg)

Historically, if you were late in filing your VAT return or in making payment to HMRC more than once in a 12-month period then HMRC would apply a surcharge on the associated liability however, if there was no liability then there was no surcharge (although defaults could impact the level of surcharges on future returns, up to 15%).

For VAT periods starting on or after 1 January 2023, HMRC has abolished the old surcharges and changed the way penalties are applied to late returns and replaced them with a penalty points system.

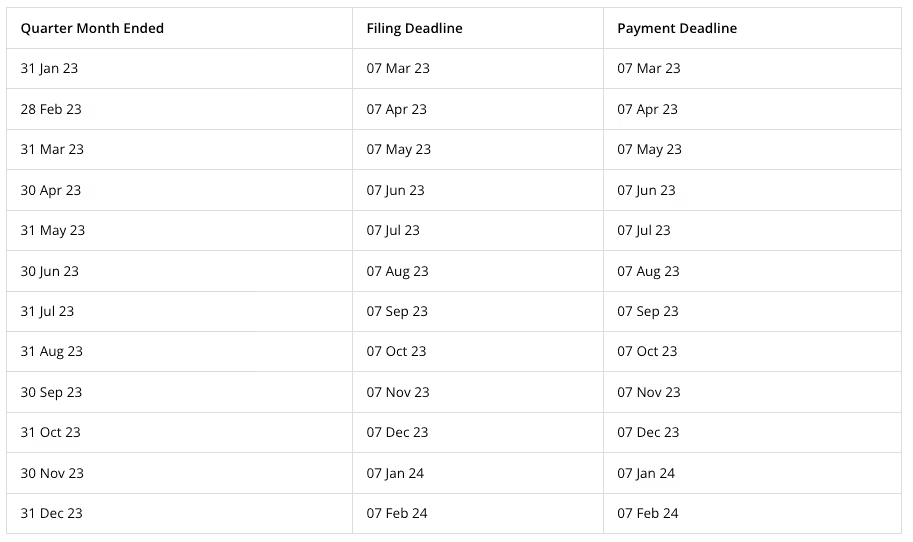

VAT filing/payment deadlines

The deadline for filing your VAT return and making any payment to HMRC has not changed. This will always be 1 month + 7 days after the end of the VAT return, i.e. a VAT return ending 31 March will have a deadline of 7 May.

Late filing of a return

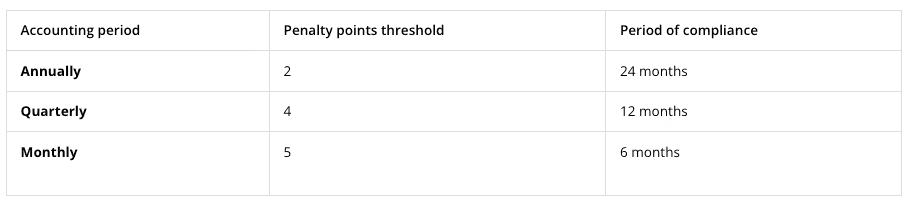

For each return you submit late, you will receive a penalty point.

Once you’ve reached your penalty point threshold, you’ll receive a £200 penalty and a further £200 penalty for each subsequent late submission while you’re at the threshold.

What is my threshold?

The threshold period is set by your accounting period and the points threshold depends on the frequency of your VAT submissions.

Late payment charges

HMRC has now separated the interest and penalty charges in an effort to simplify things.

Interest

If you pay your VAT liability late HMRC will charge interest at 2.5% over the Bank of England base rate from the first day your payment is overdue until the day it’s paid in full.

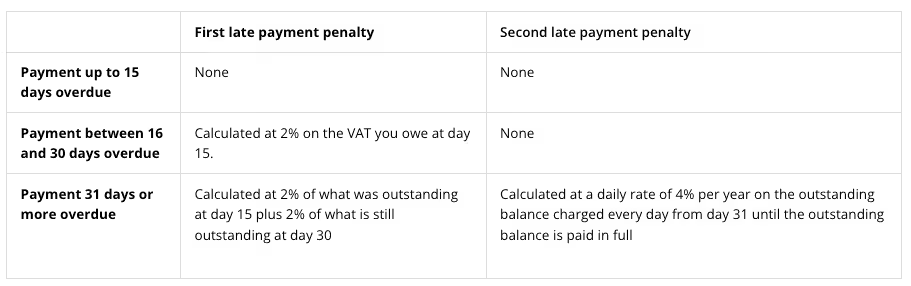

Penalties

If your payment becomes overdue by 16 days or more HMRC will impose a first late payment penalty.

When your payment is 31 or more days overdue, you get a larger first late payment penalty and a second late payment penalty.

For full details on the changes to the VAT penalty regime please see the following links:

Late payment of your VAT liability

Disclaimer.

This article has been prepared for information purposes only. Formal professional advice is strongly recommended before making decisions on the topics discussed in this release. No responsibility for any loss to any person acting, or not acting, as a result of this release can be accepted by us, or any person affiliated to us.

.jpg)

.jpg)

.svg)

%201.svg)