.svg)

When a shareholder sells their shares, they are normally subject to capital gains tax on the disposal. There is however a way to undertake a company disposal and not pay any tax at all. The way to do this is to sell to an Employee Ownership Trust (EOT). EOTs were introduced in 2014 to encourage greater employee ownership of companies inspired by the John Lewis business model.

Since their introduction, popularity of this business model has been gaining momentum with more and more companies choosing to adopt this structure. The advantages and disadvantages of this sale structure are summarised below.

Benefits of selling to an EOT

The key tax benefit to the selling shareholders is that the sale of their shares, subject to certain conditions will be free of capital gains tax, providing a savings of 10% to 20% on the disposal of the company depending on personal circumstances.

Some non-tax benefits include:

- A market for the shares is created whereas there may otherwise not be a wiling purchaser.

- The benefit of handing your business to a trusted workforce and empowering the people that you have likely worked with for many years.

- The sale process can be less stressful than a full third-party sale, given the employees, who may be part of the EOT board, should know the business well.

- The Seller can maintain a non-controlling shareholding if they wish, but this may not be desirable.

Employee benefits

The key tax benefit to the employees is that tax (but not national insurance) free bonuses can be paid up to £3,600 to each employee per tax year.

Some non-tax benefits include:

- Motivation to contribute to the business from essentially being a part owner.

- The structure does not require any capital contribution by the employees, as the company itself will normally fund the sale.

- There is no financial downside, only upside from the employees’ perspective.

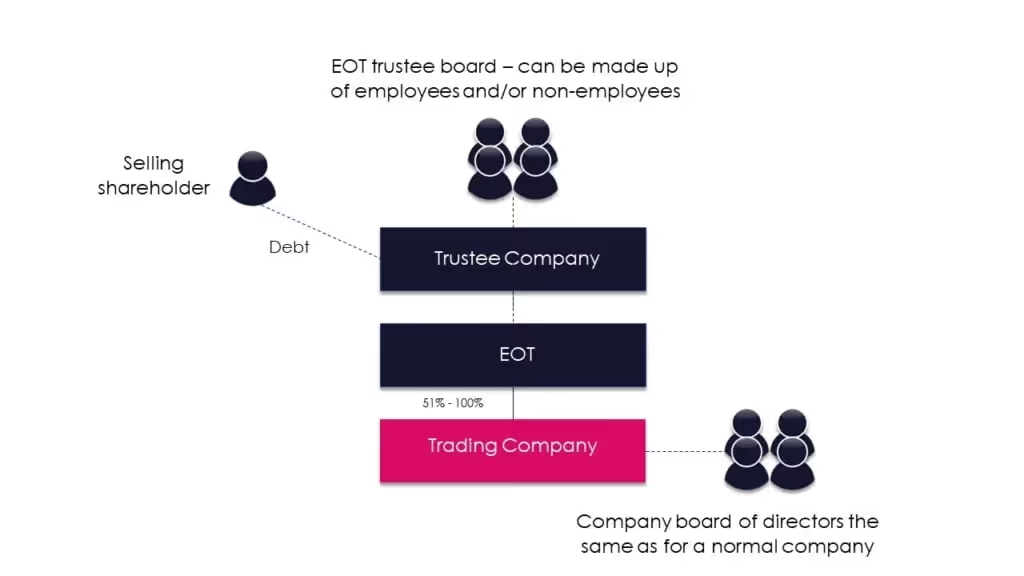

Basic structure

The diagram below shows a simplified schematic of a typical EOT structure.

Key conditions

To qualify for the beneficial tax reliefs available when transitioning to an EOT, the following conditions must be satisfied:

- A controlling interest in the company must be sold to the EOT.

- The company must be substantially a trading company or the parent of a trading group.

- All employees must benefit from the EOT on broadly similar terms, not just select employees.

- The number of continuing shareholder/directors together with certain associated persons must not exceed 40% of the total number of employees of the company/group.

Disadvantages

The following disadvantages apply to the adoption of an EOT structure:

- The seller may not get the bulk of the sale funds until the company has earned enough profits post sale to pay out the seller, but external financing can assist with this.

- If the EOT loses its controlling interest in the company and/or is wound-up in the future significant tax charges can arise.

- Generally, only one disposal to the EOT can qualify as tax-free, so if shares are retained by the original shareholders they will not likely qualify for relief when disposed of.

If you would like to find out how we can help please contact Martin Adams at martin.adams@ballardsllp.com or on 01905 794 504.

.jpg)

.svg)

%201.svg)