.svg)

If a company (or partnership with a corporate partner) owns any residential properties it will need to consider whether the Annual Tax on Enveloped Dwellings (ATED) rules apply to it.

ATED is charged on these entities when they hold an interest in any UK residential properties (dwellings) with a value that exceeds £500,000. The property value is assessed at either a valuation reference date or the purchase/development date, if later.

The current valuation reference date is 1 April 2017 but from April 2023 onwards ATED will be based on the property value at 1 April 2022. ATED is reported and paid in advance. So, for the 2022/23 tax year a return and any ATED tax charge needs to be filed and paid to HMRC by 30 April 2022.

Commercial properties are exempt from the ATED regime. These include hotels, accommodation for boarding schools, hospitals, student halls, care homes, military accommodation, and prisons. Note however that residential properties used as furnished holiday lets are not exempted from the ATED regime.

Reliefs

Relief from an ATED charge is available if the property is used for the following purposes;

- Property rental business; let to a third party on a commercial basis

- Dwellings open to the public for at least 28 days a year

- Property developers

- Property traders

- Financial institutions acquiring dwellings as a result of lending money

- Occupation by certain employees or partners

- Farmhouses occupied by a farm worker

- Providers of social housing

Relief cannot be obtained if the dwelling is occupied by a non-qualifying person, even if the occupier is paying full market rent.

A non-qualifying person is broadly an individual who is connected to the company. These include the shareholders of a company and their relatives, spouse/civil partner.

An ATED return must still be filed by the appropriate deadline in order to claim the applicable relief.

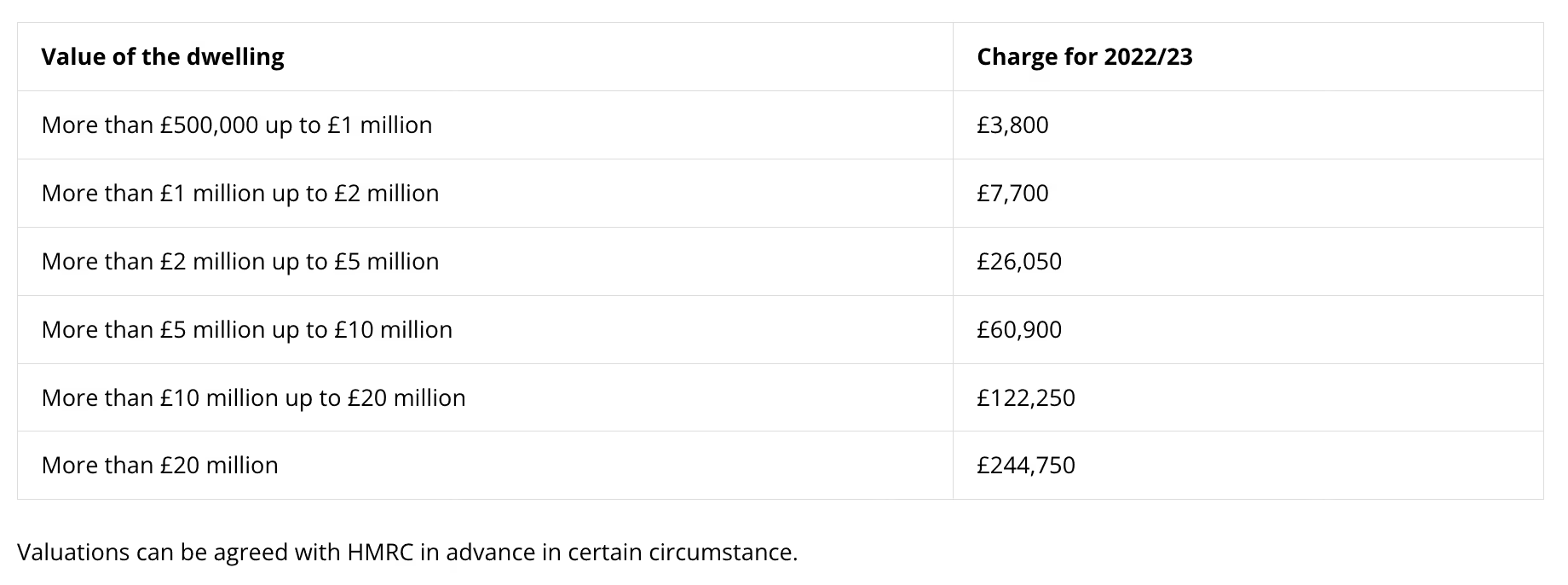

ATED Charge

Unless an ATED relief applies, an ATED charge will be payable. The quantum of this charge is dependant on the valuation band the property falls within.

The value bands and ATED rates from 1 April 2022 are as follows:

Reporting requirements

An annual ATED return will be required by 30 April at the start of the tax year if a dwelling is owned on the first day of the chargeable period (1 April each year). For example, a return for 2022/23 must be filed by 30 April 2022.

For dwellings purchased/constructed within a tax year the reporting deadline is 30/90 days respectively following the completion of those events.

A return must also be filed if you are claiming a relief within the same timescales.

Penalties will arise if returns (including relief returns) are not filed on time.

%20(1).jpg)

.jpg)

.svg)

%201.svg)